Wednesday, April 15, 2020

Thursday, August 29, 2019

云顶大妈GENM 第二季暂时过关!

-相信2019全年营业额将会突破10 billion大关,首半年已达5.25 billion.

-暂时看不到税务提高对她到底有多大影响,等2019全年业绩再来观察

-Gaming和non-gaming revenue比例进一步乖离,non-gaming比例持续缓慢走高

-Finance cost 大幅升高,值得留意!

-Tax incentive的缘故,这季的Taxation明显低很多,假设排除这incentive,net profit将进一步萎缩,对比去年同期没增长,甚至小幅下挫

-6仙股息还是值得小小的安慰

-没炸弹已经是不幸中的大幸了(暂时安全)

-虽然营业额每年增长,但是EPS却是停滞不前!(又怪Accounting Practice? 🤣)

Tuesday, April 9, 2019

为何皇帽会超越喜力?

喜力 HEINEKEN 一直以来都是超越皇帽CARLSBERG,股价亦是。

但是近来皇帽已经悄悄超越了喜力。

为何?

答案应该就在以下图表里:

实力超越对手,股价超越对手

铁证的事实和数据

但是近来皇帽已经悄悄超越了喜力。

为何?

答案应该就在以下图表里:

实力超越对手,股价超越对手

铁证的事实和数据

Monday, April 1, 2019

Tuesday, March 26, 2019

SCGM来红- 等待是一门能耐训练

- 它的最大隐忧莫过于它的贷款,第三季度又增加了接近4百万大洋的借贷。

- 这些贷款利息开销不是开玩笑的。

- 折旧开销还不需要那么担心,毕竟这笔款项不是钱不见,只是账目上的数字罢了。

- 营运开销相信是搬运期间所蒙受的开销,并不是长久的 (目前还在搬着)。

- 至于高原料价格,对比去年同期,原料价格明显回落,所以所谓的高原料价格是如何解释?

- 营运现金流吃紧,很不健康。相信所收到的钱都拿去还贷款了

其实,说真的,还有排等,问题来了,等候真的会等到春天吗?

绝对是个共患难时期,小股东有必要陪伴么?大家自行定夺吧!

Friday, March 22, 2019

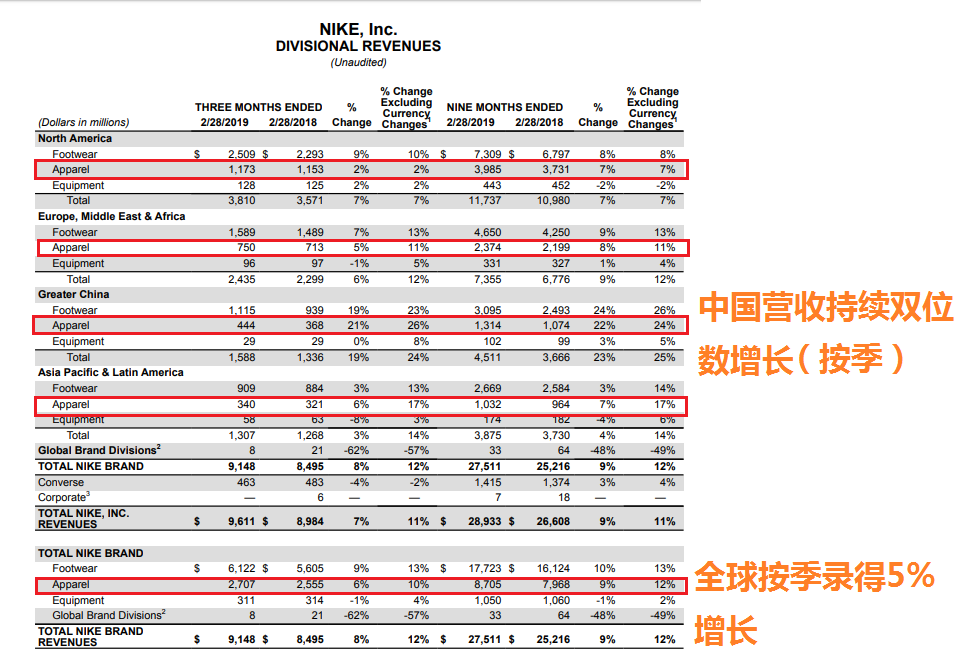

追踪成衣需求- 耐克 NIKE

作为NIKE 成衣代工之一的MAGNI,对NIKE成衣的需求足以直接或间接影响MAGNI的订单和营收。

NIKE刚刚出炉的Q3业绩显示成衣需求依旧,中国大陆方面持续录得双位数增长。与上季度Q2同样保持同等涨幅。

美国方面的营收下滑是个隐忧。

从MAGNI 2018年报里可以看到,销售至中国按年大幅增长,这也足以印证NIKE在中国的销售额相比其他区域录得大幅度提升的情况。

从MAGNI 2018年报里可以看到,销售至中国按年大幅增长,这也足以印证NIKE在中国的销售额相比其他区域录得大幅度提升的情况。

中美贸易战会否影响这个趋势?

NIKE刚刚出炉的Q3业绩显示成衣需求依旧,中国大陆方面持续录得双位数增长。与上季度Q2同样保持同等涨幅。

美国方面的营收下滑是个隐忧。

中美贸易战会否影响这个趋势?

Subscribe to:

Posts (Atom)